The Wrong Shelf: How Regard’s Positioning Put an $81M Company in a $5.3B Fight

That's a lot of green.

Question of the day: What do you call a company with 10 million accepted AI diagnosis recommendations competing for deals against ambient scribes that have never recommended a single diagnosis?

You call it Regard.

And right now they’re in a $5.3 billion fight they didn’t need to enter.

Regard has raised $81 million. Penn Highlands Healthcare reported a $7 million revenue increase after deploying the platform. Sentara Health scaled to all 12 hospitals after seeing 2 to 4x ROI and 65 to 75 percent physician adoption. Cedars-Sinai was so convinced that they became both an enterprise customer and a Series B investor.

By every product metric that matters, Regard is winning. THEY ARE WINNING.

But here’s what I can’t stop thinking about (not Severance the show this time). In the last four years, Regard has publicly renamed itself at least four times.

2021 to August 2023: “AI co-pilot for physicians.”

March 2024: “AI clinical insights platform” and “clinical automation” running simultaneously in the same press cycle.

Early 2025: “AI clinical automation technology.”

Mid 2025: “AI-powered Proactive Documentation platform.”

Four names. Four years. And for a stretch in 2024, two names at the same time. Each one a press release, a homepage redesign, a sales team learning new language, a market that has to re-learn what Regard is.

That’s not iteration, my friends.

The pattern suggests they’re searching for a category frame in public without having done the upstream positioning work that would make the name obvious.

If you’ve ever lost a bake-off where the buyer never really understood what you were, this is that problem at Series B scale. With $81 million behind it.

And the cost of that search? It’s not abstract. It shows up in how buyers compare you. How investors value you. How many deals do you lose before you even get to demo. So I’m going to walk through every piece of it.

If you’re a Series A or B or C healthcare SaaS founder, the pattern is going to look uncomfortably familiar. Because this isn’t a Regard problem.

It’s the default state of positioning in healthcare SaaS. Regard is just the most visible example. Buckle up.

But First: The Smartest Positioning Move in Healthcare AI

Before I get into the diagnosis, I need to steelman Regard. Because they actually made the single smartest positioning move in healthcare AI in 2025, and almost nobody talked about it.

In October 2025, Regard announced an integration with Microsoft Dragon Copilot (that’s Nuance’s ambient AI platform). Instead of competing head-to-head with the $5.3 billion scribe category, Regard partnered with the biggest scribe in the market.

Think about what that integration says about what Regard actually is. Nuance Dragon Copilot handles the conversation. Regard handles the chart. The scribe captures what the doctor says during the visit. Regard analyzes what’s in the record before the visit. They’re complementary, not competitive.

The Dragon Copilot integration is Regard’s positioning, expressed in product strategy, perfectly. It says: we’re not a scribe. We’re the intelligence layer that runs before the scribe turns on.

But the homepage still says “Proactive Documentation.”

The product strategy knows what Regard is. The positioning language doesn’t. And that gap is what the rest of this article is about.

Positioning Is Not Messaging (and This Distinction Is Worth $81M)

Most founders treat positioning as a messaging exercise. New tagline. Refreshed homepage. Maybe a category name that sounds good in a TechCrunch headline.

That’s backwards. BACKWARDS IS NOT FORWARDS.

Positioning is the strategic decision about what you are, who it’s for, and what shelf the buyer puts you on when they’re comparing options. Messaging is how you communicate that decision after you’ve made it. When you skip the strategy and jump to the words, you end up doing what Regard has done.

Ahem. Changing the words every 12 months because the underlying decision was never made.

So the words keep changing. And the market keeps getting confused.

April Dunford’s framework breaks positioning into components that build on each other:

Competitive alternatives

Unique capabilities

Differentiated value

Target segments

Market category.

There’s also another piece that is wildly underused: the buyer’s own language. What your customers say about you in reviews and case studies and testimonials is almost always a better articulation of your value than what your marketing team writes.

The gap between what the company says and what the buyer says is the positioning gap. And it’s visible to anyone willing to look.

So let’s dive in.

Walking Regard Through the Positioning Framework

I use a seven-component walkthrough with every healthcare SaaS company I work with. I’m going to run Regard through it using nothing but public data.

To be clear, this isn’t a critique. The Regard team has built something genuinely rare. This is a diagnosis of the research I’ve done. And what I’ve learned from it.

1. Product Context: What’s Changing and Why It Matters Now

The market context for Regard is actually amazing. 97% of patient data goes unused at the point of care (pulled from World Economic Forum data). EHRs have become data graveyards. They store everything. Surface almost nothing. A single patient record contains an average of 50,000 data points, and clinicians review roughly 3% of that during a visit.

That’s wild. And it’s the kind of number that should be on Regard’s homepage in giant font.

To be fair, the 97% stat does appear on Regard’s site. But it’s buried in a blog post and secondary pages, not leading the hero. The homepage leads with: “Proactive Documentation to transform care.”

Now compare that to what Regard’s CEO Eli Ben-Joseph says in interviews: “97% of data in a chart does not get seen by a doctor on an average visit.”

That’s a specific urgent number. It creates immediate tension. And it’s not the first thing a visitor sees. The CEO is doing better positioning in a podcast than the homepage is for every visitor.

2. Problem Framing: The Buyer’s Language vs. the Company’s Language

Here’s what Regard’s actual customers say about the product:

Dr. Colin Findlay at Sentara Health says the platform shows him information in the chart he would not have found on his own. Information that is sometimes critically important and completely changes the course of management.

A rural hospital executive says rural hospitals run lean. If you can improve case mix index to capture revenue you’re actually earning, that’s what keeps you afloat.

Penn Highlands Healthcare reported outcomes: $7 million revenue increase. 30% time savings. ROI of two to four times the cost of the tool, depending on the facility.

So the buyers talk about three things. Missed diagnoses that get caught. Revenue that gets recovered. And survival economics for smaller hospitals (this is a small sample size from buyers).

The buyers are talking about finding things doctors miss and recovering millions in revenue. The company is talking about unifying teams and generating documentation.

Those are not the same story.

3. Competitive Alternatives: What the Buyer Actually Tries Instead

This is where Regard’s positioning problem becomes structural. And where the economics start to compound.

When a buyer evaluates Regard, what are they actually comparing it against? Not what Regard thinks. What the buyer is currently doing instead.

The EHR itself. Epic and Oracle Health have built-in analytics and clinical decision support modules. They don’t do what Regard does. But the buyer’s first question is always, “Can’t our EHR handle this?” If your positioning doesn’t immediately answer that question, you’ve already lost momentum in the deal.

AI ambient scribes. This is the big one. Abridge ($5.3 billion valuation, $100 million ARR, 150+ health systems). Ambience Healthcare ($1.25 billion valuation, $345 million raised). Microsoft-owned Nuance DAX. These companies capture what the doctor says during a visit and turn it into a note. That’s fundamentally different from what Regard does. But by adding ambient scribe functionality and positioning as a “documentation platform,” Regard has voluntarily placed itself on the same shelf.

CDI teams. Clinical documentation improvement specialists who manually review charts after discharge. They’re slow, expensive, and they catch a fraction of what Regard catches. But they’re the status quo in most health systems.

Doing nothing. The physician reviews what they can. Misses what they miss. And the hospital never knows what revenue it left on the table.

You define competitive alternatives by what the buyer would use if your product didn’t exist. Regard’s real alternative isn’t Abridge. It’s the CDI team plus the physician reviewing 3% of data manually.

But Regard’s current positioning puts them on the same shelf as the scribes. And that shelf is super expensive to compete on.

4. The Shelf Problem (or: What Competing Against $5.3 Billion Looks Like)

Let me make the economics as clear as possible because this is where “positioning is a business decision” stops being theory.

Abridge: $758 million raised. $5.3 billion valuation. $100 million ARR. Backed by a16z and Khosla. 150+ health system deployments.

Ambience: $345 million raised. $1.25 billion valuation. Backed by a16z and OpenAI. Cleveland Clinic, UCSF Health, Houston Methodist.

Regard: $81 million raised. $350 million valuation.

When Regard positions itself as a “documentation platform,” it enters every buyer conversation carrying the burden of these comparisons. Not because the products are the same (they aren’t). But because the category frame triggers the wrong competitive set in the buyer’s mind.

The buyer thinks: “We’re evaluating documentation AI. Abridge does documentation. Ambience does documentation. Regard does documentation. Let me compare these three.”

And suddenly, Regard is in a three-way comparison where the other two companies have 4 to 9x the funding, massive brand recognition, and the dominant market narrative. The thing that makes Regard genuinely different (pre-encounter diagnostic synthesis from chart data) isn’t even the axis of comparison.

That’s what default positioning costs. Not a failed homepage test. A structural competitive disadvantage that shows up in every deal, every investor conversation, and every press mention.

5. Unique Capabilities: What Regard Can Do That Scribes Structurally Cannot

Here’s where Regard actually wins. And where the positioning gap is.

Ambient scribes start when the conversation begins. They listen to what the doctor says and document it. Abridge and Ambience are very good at this.

Regard starts before the conversation begins. It analyzes the entire patient chart (all 50,000 data points that the doctor won’t have time to review) and surfaces missed diagnoses, relevant lab trends, medication conflicts, and documentation gaps before the physician walks into the room.

Ben-Joseph has said publicly that the diagnosis recommendation is at the core of what Regard does. And that almost no other company attempts it because of how difficult it is. It requires making sense of massive amounts of clinical data and applying medical reasoning at scale.

That’s not a feature advantage. It’s a structural capability difference. A scribe cannot recommend a diagnosis because a scribe only processes what the doctor says.

Regard processes what’s in the chart.

Ten million accepted diagnosis recommendations. That number means physicians reviewed what Regard surfaced, agreed with the clinical reasoning, and acted on it. Ten million times.

But on the homepage? It’s framed through the lens of “documentation.” The single most defensible capability in healthcare AI is being subordinated to a category frame that points toward Abridge and Ambience instead of away from them.

6. Differentiated Value: The Outcome Only Regard Delivers

Here’s the test: can any competitor credibly claim the same outcome?

“Better documentation.” Abridge can claim that. Ambience can claim that. Nuance can claim that. Not differentiated.

“Time savings for physicians.” Everyone claims this. Table stakes.

“Revenue impact from better coding.” CDI teams claim this. Closer but still not unique.

“Finding diagnoses your physicians are missing. Conditions that would have gone undetected. Which directly recovers revenue and improves patient safety.”

No ambient scribe can claim this. None. The clinical outcome and the financial outcome are both downstream of the same unique capability: diagnostic synthesis from chart data.

Penn Highlands didn’t report a $7 million revenue increase because Regard wrote better notes. They reported it because Regard found conditions (hypertension, malnutrition, sepsis risk) that would have gone uncoded because the physician didn’t have time to find them in the chart.

That’s the differentiated value. And right now it’s being filtered through a category frame that obscures it.

7. Market Category: The Shelf You Put Yourself On

Regard has invented a category name: “Proactive Documentation.”

The problem with this term is that it anchors to something the buyer already knows (documentation) which triggers the competitive comparison we just walked through. The adjective “proactive” modifies the noun. But the noun is doing the category work.

When a buyer hears “Proactive Documentation,” they file it under documentation tools. And then Abridge and Ambience are on the same shelf.

The market category’s job is to point the buyer toward your differentiated value. “Proactive Documentation” points toward documentation quality. Regard’s differentiated value is diagnostic intelligence and revenue recovery from conditions that would otherwise go undetected.

Those are different shelves. And the shelf you choose determines which competitors you face, which budget you pull from, and which stakeholder makes the buying decision.

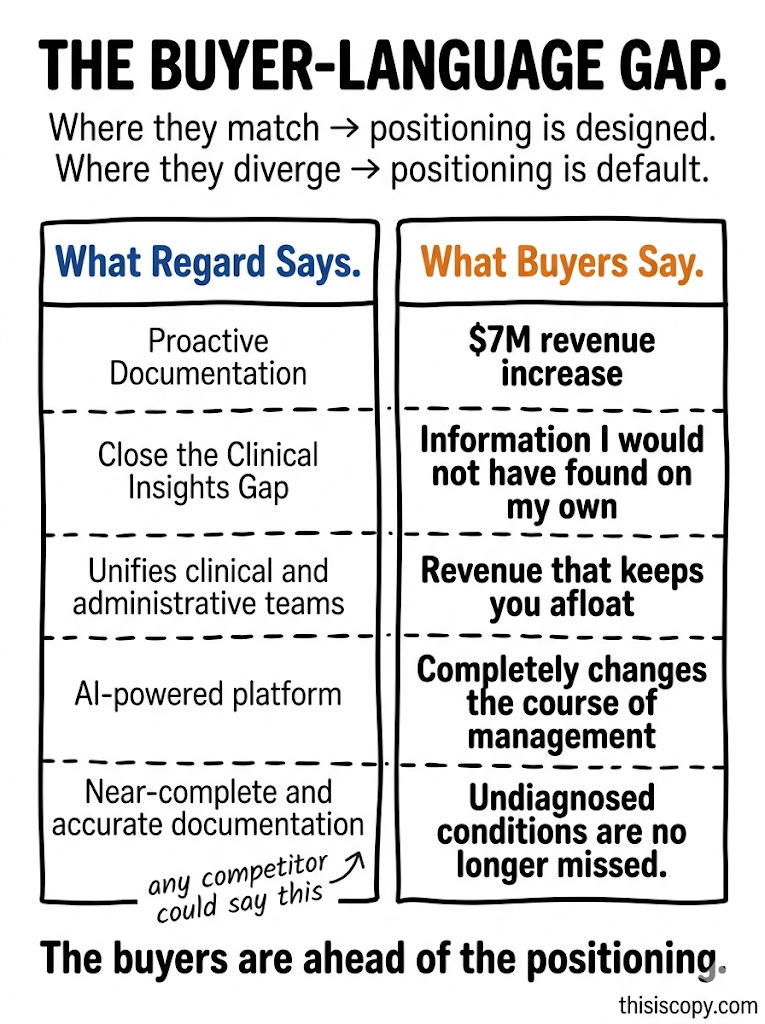

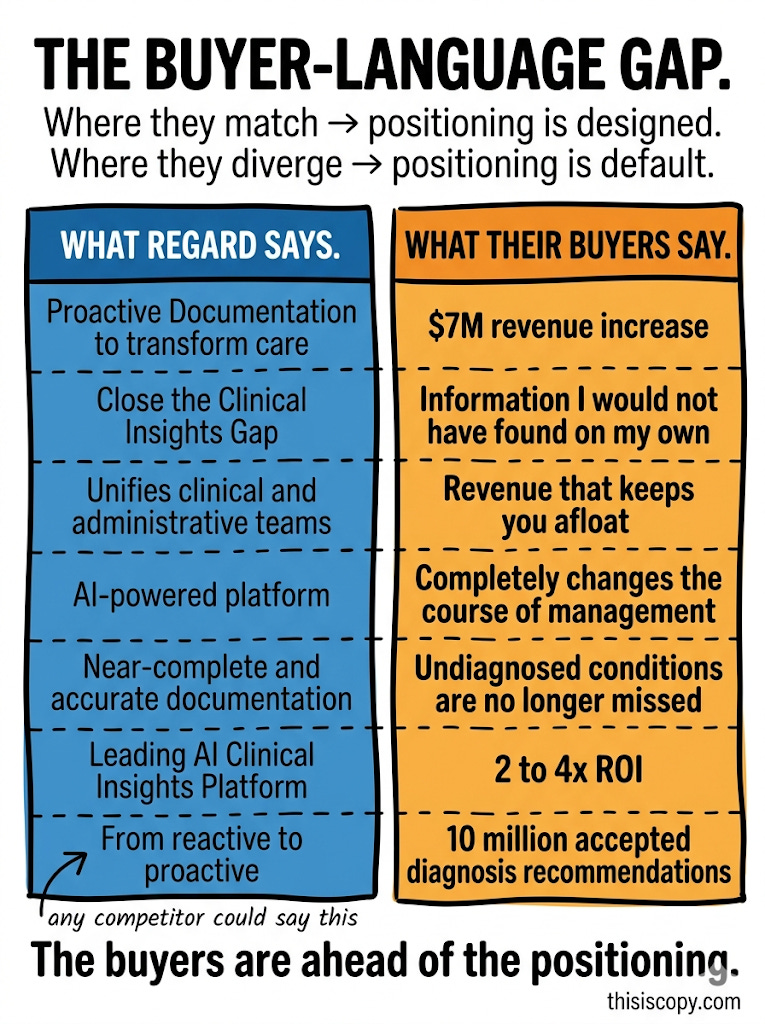

The Buyer-Language Gap (This Is the Whole Article in One Table)

I call this the Buyer-Language Gap. It’s a diagnostic I run with every company I work with, and it makes the positioning gap undeniable. You put company language on the left and buyer language on the right. Where they match, positioning is designed. Where they diverge, positioning is default.

For Regard, they diverge everywhere.

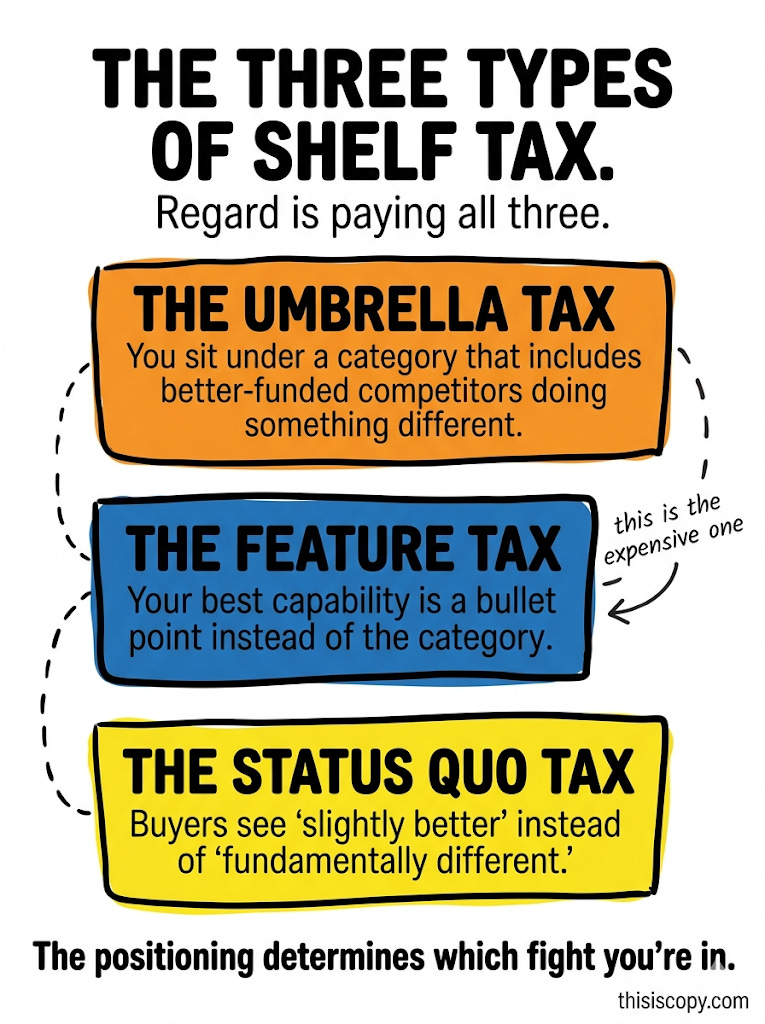

The Three Kinds of Shelf Tax (and Regard Is Paying All of Them)

I want to name what’s happening here because I think it applies to way more companies than Regard.

I call it the Shelf Tax. It’s the cost you pay when your positioning puts you on the wrong shelf in the buyer’s mind. And after looking at this pattern across dozens of healthcare SaaS companies, I see three distinct types.

1. The Umbrella Tax. You position under a broad category (like “documentation”) that includes well-funded competitors who do something adjacent but fundamentally different. Regard leads with “Proactive Documentation,” which puts them under the same umbrella as Abridge, Ambience, and Nuance. The buyer compares them all on the same axis. Regard’s actual differentiation never enters the conversation.

2. The Feature Tax. Your most defensible capability gets described as a feature of a category instead of the defining attribute of a different category. Regard’s diagnosis recommendation engine (10 million accepted recommendations) is treated as a feature of a documentation platform. Instead of defining the category, it’s a bullet point on a features page. The most important thing the product does is positioned as a secondary benefit.

3. The Status Quo Tax. Your positioning doesn’t clearly separate you from the manual process you replace. CDI teams are the real status quo Regard displaces. But because the positioning anchors to “documentation” instead of “diagnostic intelligence,” buyers evaluate Regard as “slightly better than what we have” instead of “fundamentally different from what we have.” That’s the difference between a nice-to-have and a must-have.

Regard is paying all three simultaneously. And the math looks something like this.

Let’s Do Some Math

Say Regard runs 100 qualified opportunities through the pipeline in a year. If 30% of those deals stall or die at the “so how are you different from Abridge?” question (because the positioning invited the comparison), that’s 30 opportunities lost before Regard even gets to show what makes them different. At a $100K ACV, that’s $3 million in pipeline evaporating at the wrong stage for the wrong reason.

Not because the product lost. Because the frame lost.

That’s the Shelf Tax. And it compounds in every direction. Compressed valuations (investors apply category multiples instead of premium multiples when they can’t immediately articulate your differentiation). Elongated sales cycles (every meeting spent explaining “how we’re different from Abridge” is a meeting not spent closing). Competitive losses on the wrong axis. And category consolidation risk (the market starts saying “Abridge and others” and if Regard is in that “and others” bucket, the positioning gap becomes permanent).

This is what I mean when I say positioning is a business decision, not a marketing exercise. The words on the homepage aren’t just copy. They’re the thing that determines which competitive fight you’re in, which budget you pull from, and how investors price your differentiation.

The Opportunity on the Other Shelf: $4.2 Billion and Growing

So the Shelf Tax shows you what default positioning costs. But here’s what makes the Regard story super interesting: the right shelf isn’t just less expensive to compete on.

It’s dramatically bigger. Like as dramatic as Goodwill Hunting (a really good movie).

The clinical documentation improvement market is a $4.2 billion industry (GMI, 2023 data) growing at 7.3% annually. That’s the money currently going to CDI teams, CDI software, outsourced CDI services, and revenue integrity programs.

It’s also the budget that exists because hospitals know they’re missing diagnoses and leaving revenue on the table.

There are roughly 6,100 hospitals in the US (AHA data). The average CDI specialist earns $80,000 to $135,000 depending on experience and certification. Most hospital CDI teams run 3 to 5 specialists. That’s $300,000 to $675,000 per hospital per year in CDI labor alone, before software and outsourced services.

And here’s the thing: the 2024 MDaudit Benchmark Report puts the total “at-risk” revenue from coding inaccuracies at $11.2 million per healthcare organization. CDI teams exist to close that gap. They catch some of it. They miss a lot.

Regard’s pitch on the documentation shelf: “We’re like Abridge but we also do some stuff before the visit.” That’s a feature comparison against $5.3 billion in funding.

Regard’s pitch on the diagnostic intelligence shelf: “Your CDI team costs $400K a year and catches a fraction of the missed diagnoses. Regard analyzes 100% of the chart, recommends diagnoses before the visit, and Penn Highlands saw $7 million in recovered revenue. Would you like to augment your CDI program or replace parts of it entirely?”

That’s not competing for the documentation AI budget. That’s competing for the revenue integrity budget. Which is 3 to 5x larger and has completely different buyers (CFO, VP Revenue Cycle, CMO) than the IT and digital health teams currently evaluating documentation tools.

And there’s a third angle (before I need more coffee) that makes the opportunity even bigger: the complementary sale.

If Regard positions itself as diagnostic intelligence that runs before the scribe, every hospital that buys Abridge or Ambience is a potential Regard customer too. Not a competitor. A warm lead. The Dragon Copilot integration already proves this works in practice.

But the positioning language needs to make it obvious to every buyer, not just the ones who stumble into the integration page.

What Designed Positioning Would Look Like

I’m not going to write Regard’s full positioning for them in a Substack article (good positioning requires internal knowledge about sales conversations, competitive losses, and strategic priorities that aren’t visible from outside).

But I can point to where every component of the framework is pointing. And it’s all pointing in the same direction. Away from documentation. Toward something like this:

The candidate shelf: Pre-Encounter Diagnostic Intelligence.

Not “Proactive Documentation.” Not “clinical insights.” A category frame that does three things at once: it tells the buyer when Regard’s value happens (before the encounter), what it actually does (diagnoses, not documentation), and why it’s structurally different from scribes (intelligence from chart data, not transcription from conversation).

Here’s what the homepage hero could sound like under this frame:

“Your doctors review 3% of the chart. Regard reviews 100%. Before the patient walks in, Regard surfaces the diagnoses your physicians would have missed.”

And the proof points reframe too:

“10 million accepted diagnosis recommendations” (not “documentation generated”)

“$7M in recovered revenue from conditions that would have gone uncoded” (not “time savings”)

“65-75% physician adoption because it changes clinical decisions” (not “ease of use”)

Same product. Same data. Completely different shelf. And on this shelf, Abridge and Ambience aren’t competitors. They’re complementary. Which is exactly what the Dragon Copilot integration already proves.

I want to be clear: “Pre-Encounter Diagnostic Intelligence” is a directional candidate, not the final answer. The right name comes from doing the full positioning work with the team. But every piece of the framework points away from “documentation platform” and toward something no ambient scribe could credibly claim.

Three Questions Regard Can Answer From Internal Data Tomorrow

Question 1: In your last 20 closed-lost deals, how many times did the buyer compare you to Abridge, Ambience, or Nuance? If the answer is more than 30%, the Umbrella Tax is real and it’s quantifiable. Multiply that percentage by the total pipeline value of those deals. That’s your annual Shelf Tax in dollars.

Question 2: In your last 20 closed-won deals, what did the champion say was the reason they chose Regard? Pull the actual quotes from call recordings or emails. If the buyers say “diagnoses” and “revenue” and “conditions we would have missed,” but the sales deck says “documentation” and “time savings,” the Buyer-Language Gap is confirmed from inside the building.

Question 3: Which budget did the deal come from? If Regard is being purchased from the digital health or IT innovation budget, they’re on the documentation shelf. If the deal comes from the revenue cycle or clinical operations budget, they’re on the diagnostic intelligence shelf. The budget source tells you which shelf the buyer put you on regardless of what the homepage says.

These three questions take a week to answer. And the answers will either confirm every section of this article or prove me wrong. Either way, the data is already in the CRM.

What I Might Be Wrong About

I want to be honest about the limits of this analysis. My frail human mind.

I’m working from public data. I can see the homepage, the press releases, the customer quotes, the funding rounds, and the CEO’s interviews. I can’t see the pipeline. I can’t see the win/loss data.

But I can’t see the internal sales conversations or the board deck.

It’s possible that Regard’s naming changes were deliberate responses to buyer feedback that I can’t observe from my eyeballs.

It’s possible the “Proactive Documentation” frame performs better in sales conversations than it reads on the homepage. It’s possible the team has already identified everything in this article and is actively working on it.

And it’s possible that the documentation shelf, despite the competitive intensity, is strategically correct for Regard at this stage because that’s where the current budget exists, and the diagnostic intelligence shelf doesn’t have an established buying motion yet.

These are real counterarguments. The three internal questions above would resolve them. I’d genuinely love to be wrong about some of this, because Regard has built something that deserves to win on its own terms.

The Shelf Tax Diagnostic: Run This On Your Own Pipeline

If you’re a healthcare SaaS founder between Series A and C, here’s how you calculate your own Shelf Tax. It takes about a week.

Step 1: Pull your last 20 closed-lost deals. Count how many times the buyer compared you to a company that does something fundamentally different from what you do. That’s your Wrong-Shelf Rate.

Step 2: Multiply your Wrong-Shelf Rate by the average deal value of those lost opportunities. That’s your annual Shelf Tax in dollars. If your Wrong-Shelf Rate is 30% and your average deal was $100K, you’re paying a $600K Shelf Tax on just 20 deals.

Step 3: Look at the competitive alternative the buyer actually compared you to. If you win on that axis, great, you’re on the right shelf. If you lose on that axis but win on a different one, you’re paying the Shelf Tax. And the fix isn’t better selling. It’s better positioning.

Run this before you finish your coffee. If the number makes your stomach drop, we should talk.

Why You Should Care Even If You’re Not Regard

If you’re a Series A or B healthcare SaaS founder, here’s the uncomfortable question: Does your homepage (or on a broader level, your messaging as a whole) describe what your product uniquely does? Or does it describe a category your product happens to be in?

And does that messaging (foggy clarity) trickle down your landing pages and emails?

Because the pattern I just walked through with Regard isn’t unique. It’s the default state of positioning in healthcare SaaS between Series A and C. The company builds something genuinely differentiated. The marketing team describes it in category terms because that’s “what buyers search for.” And the positioning defaults to whatever shelf the market puts you on.

The cost compounds silently. You don’t see the deals you lost because the buyer filtered you out before the demo. You don’t see the investor who valued you at category multiples because your differentiation wasn’t visible in the first 90 seconds. You don’t see the press coverage that lumped you in with three competitors because your own homepage used the same language they use.

The fix isn’t a new tagline. It’s not a homepage refresh. It’s the upstream strategic work of deciding what you are (walking through competitive alternatives, unique capabilities, differentiated value, and market category in order) and then letting that decision drive every word on every page.

Your buyers already know what makes you different. It’s in their reviews. Their case study quotes. Everything they say about the product.

The positioning work isn’t an invention. It’s listening to what they’re already saying and putting it in the right place.

I help Series A-C healthcare SaaS companies close the gap between what their product actually does and what their homepage and messaging says. From product positioning to messaging.